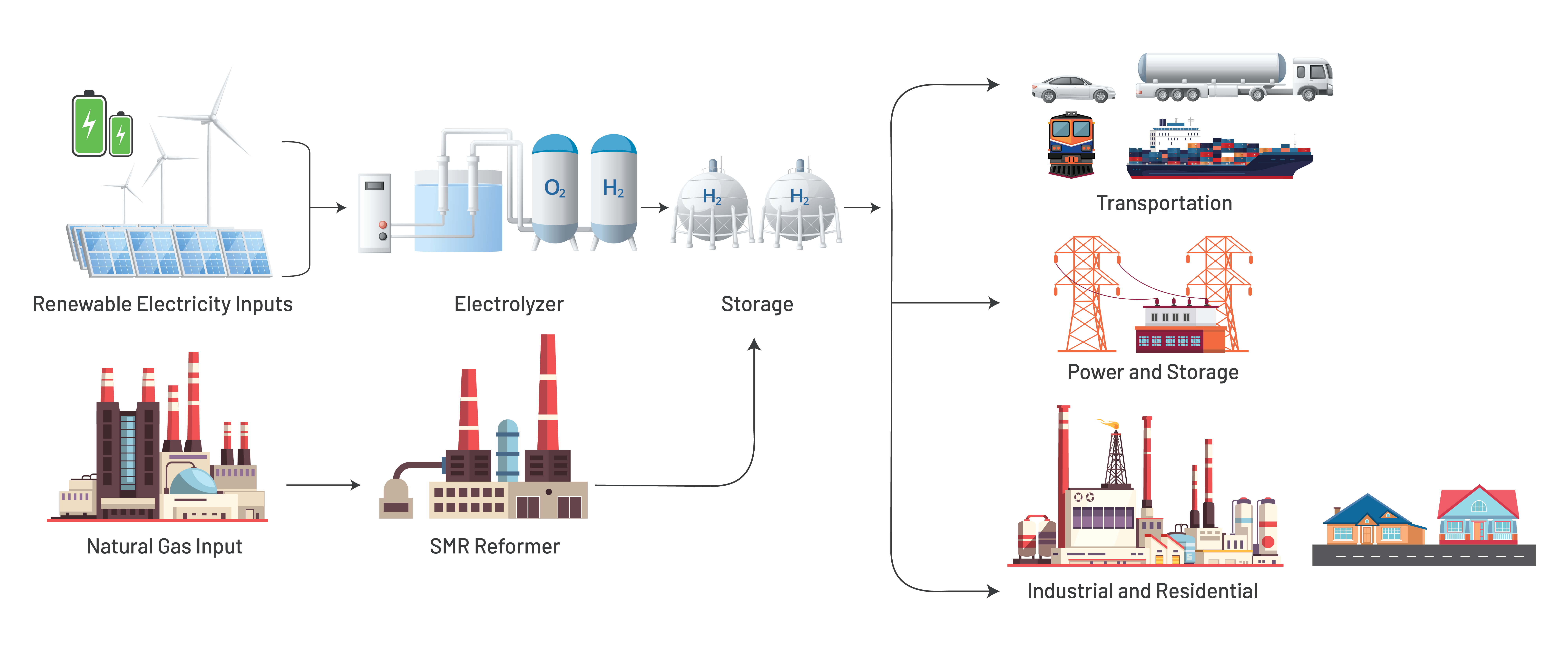

Green hydrogen is another low-carbon hydrogen solution, using electrolysis to divide the water molecule H2O into its hydrogen and oxygen elements. While green hydrogen production is more energy-intensive than blue hydrogen production, it can be less carbon intensive if the electricity needed for the electrolysis is provided solely by solar, wind or hydroelectric power. Pink hydrogen is similar to green hydrogen in that it's generated by electrolysis but produced using low-carbon electricity caused by nuclear power.

Clean hydrogen sources like these are being reimagined by investors like Goldman Sachs, utility companies, communities, states, regions and even the federal government as a fuel source for various industries. Each method of low-carbon hydrogen production has its own benefits and challenges, and all are attracting interest because of their potential to reduce greenhouse gas emissions.

One of the many initiatives the federal government is embracing is the development of a nationwide hydrogen hub network. Congress appropriated $8 billion through the Department of Energy (DOE) for the establishment of 6-10 regional hubs, dubbed H2Hubs, to provide DOE grants for clean hydrogen in the United States under the Infrastructure Investment and Jobs Act (IIJA). In simple terms, each hub will receive between $500 million and $1 billion of DOE funding in the form of cooperative agreements and other incentives.

The development of H2Hubs is intended to be the first step toward the creation of a national network of clean hydrogen producers and customers that could help facilitate the emergence of a clean hydrogen economy. To kick off the effort, in September 2022, the DOE Office of Clean Energy Demonstrations issued DE-FOA-0002768 entitled “Regional Clean Hydrogen Hubs.” This funding opportunity announcement (FOA) called for proposals from prospective hubs.

Seventy-nine hydrogen hub proposals were submitted, with 33 of them getting an “encourage” stamp of approval from DOE to move forward in the application process. 1898 & Co. actively supported two regional hydrogen hubs in the process.

Though there is broad agreement on the need for a robust clean energy economy that includes hydrogen hubs, there is much to be considered. Here are seven key questions that industry players are considering as the clean hydrogen industry develops:

.svg)